Are FHA Loans Only for First-Time Home Buyers?

Many

people believe FHA loans are exclusively for first-time buyers.

This common misconception prevents qualified borrowers from exploring

valuable financing options. The truth is that FHA loans serve a

much broader audience than most realize.

Many

people believe FHA loans are exclusively for first-time buyers.

This common misconception prevents qualified borrowers from exploring

valuable financing options. The truth is that FHA loans serve a

much broader audience than most realize.

What Is an FHA Loan?

An FHA loan is a mortgage backed by the Federal Housing Administration, designed to help those who qualify for FHA loans. This government agency doesn't actually lend money. Instead, it insures mortgage loans made by approved lenders. This insurance protects lenders against losses if borrowers default on their payments.

The Federal Housing Administration created these loans in 1934 to help more Americans buy a home. The program makes homeownership accessible to people who might not qualify for traditional financing. FHA home loans have helped millions of families achieve their housing goals over the decades.

These mortgage products come with more flexible requirements than conventional loans. Borrowers can qualify with lower credit scores and smaller down payments. The program also accepts various income sources and allows higher debt-to-income ratios.

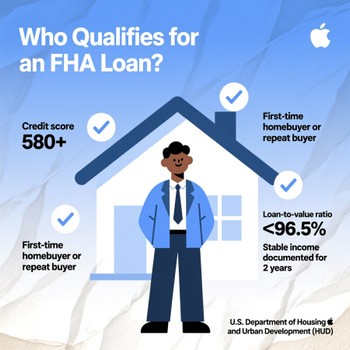

Who Qualifies for an FHA Loan?

The FHA loan program welcomes both new and experienced homeowners. First-time homebuyers often choose FHA financing because of the lower barriers to entry. However, individuals who have previously owned a home can also apply for an FHA loan.

You can use an FHA loan multiple times throughout your life. The main requirement is that you must occupy the property as your primary residence to qualify for the FHA. You cannot use an FHA mortgage to buy investment properties or vacation homes.

Previous homeowners often return to FHA financing when life circumstances change. Divorce, job relocation, or downsizing may prompt someone to sell their current home and purchase another with an FHA loan. As long as you meet the current loan requirements, you can reapply for an FHA loan.

FHA Loan Requirements for All Borrowers

The Federal Housing Administration sets specific standards for all borrowers. These FHA loan requirements apply whether you're buying your first home or your fifth. Understanding these guidelines helps you determine whether an FHA mortgage is a good fit for your situation.

Credit score requirements for FHA loans are more lenient than conventional mortgages. You can qualify for an FHA loan with a credit score as low as 580 if you make a 3.5% down payment. Borrowers with scores between 500 and 579 may still qualify, but they will need to put down a 10% down payment.

- The down payment requirement starts at just 3.5% for qualified borrowers

- FHA borrowers must pay mortgage insurance premiums throughout the life of the loan

- The property must meet specific property standards set by FHA guidelines

Income verification follows standard mortgage industry practices. Your FHA lender will review pay stubs, tax returns, and bank statements. They calculate your debt-to-income ratio to confirm you can afford the monthly mortgage payments. FHA loans typically allow debt-to-income ratios of up to 43%, although some borrowers may qualify for FHA loans with higher percentages.

Employment history is a key factor when applying for an FHA loan. Most lenders require at least two years of steady work experience in the same field to qualify for an FHA mortgage. Self-employed borrowers need to provide additional documentation. Student loans and other debts factor into your overall financial picture.

Understanding FHA Loan Limits

The FHA loan limits vary by county and reflect local housing costs. These limits change annually in response to market conditions. In 2026, the baseline limit for a single-family home in most areas is $498,257. High-cost areas have limits reaching $1,149,825.

Your location determines the specific FHA loan limits applicable to you. Urban markets with expensive real estate typically have higher ceilings. Rural areas with lower home prices have smaller maximum loan amounts. You can check the limits for your county on the HUD website.

These limits apply to the base loan amount before the addition of the upfront mortgage insurance premium. If you want to buy a home above the limit, you'll need different financing. A conventional loan or jumbo mortgage might work better for higher-priced properties.

How FHA Loans Compare to Conventional Loans

Shopping for a mortgage involves weighing various loan options, including FHA mortgage loans, which may offer more favorable terms and conditions. FHA mortgages and conventional loans serve different borrower profiles. Each program has distinct advantages depending on your financial situation.

Conventional loan requirements are generally stricter than those of the FHA standards. Most traditional lenders prefer credit scores of 620 or higher. Many require scores above 700 for the best interest rates. The standard down payment for a conventional mortgage is 5% to 20%.

Mortgage insurance works differently between these two loan types. FHA mortgage insurance includes both an upfront premium and annual premiums. You pay 1.75% upfront, which can be rolled into your loan amount. The annual mortgage insurance premium ranges from 0.45% to 1.05% depending on your loan term and down payment.

Conventional loans typically require private mortgage insurance only if the down payment is less than 20%, while FHA loans require different criteria. Once you reach 20% equity, you can cancel this insurance. FHA mortgage insurance typically stays for the life of the loan if you made the minimum down payment.

Interest rates on FHA loans are often competitive with conventional options. Your specific rate depends on your credit score, down payment, and current market conditions. A loan officer can help you compare FHA rates with other mortgage products.

First-Time Homebuyer Advantages

While not exclusively for first-time buyers, FHA loans do offer special benefits to this group. First-time home buyers often have limited savings for a down payment. The 3.5% minimum makes homeownership accessible sooner, especially for those who qualify for FHA loans. They may also have shorter credit histories, making FHA's flexible score requirements helpful.

The program defines a first-time homebuyer broadly. You qualify if you haven't owned a primary residence in the past three years, allowing you to access FHA loans for first-time buyers. This means returning buyers can sometimes claim first-time status again. Single parents who owned a home only with a former spouse also qualify as first-time buyers.

Gift funds from family members can cover your entire down payment. This policy helps first-time homebuyers who receive financial assistance from parents or relatives. The donor must provide a gift letter confirming that the money doesn't require repayment.

When to Choose an FHA Loan

Deciding between an FHA loan and other financing options depends on your personal circumstances. Several situations make FHA financing the wise choice. Evaluating your credit profile, savings, and long-term goals helps guide this decision.

Borrowers with less-than-perfect credit benefit most from FHA programs. If your credit score falls below 700, you'll likely get better terms with an FHA mortgage. The program accepts past financial difficulties more readily than conventional lenders. Previous bankruptcies or foreclosures don't automatically disqualify you.

Limited savings for a down payment make FHA loans a more attractive option. Saving 20% for a conventional mortgage takes years for many families. The lower down payment requirement allows you to get into a home sooner. You can start building equity instead of paying rent.

High debt-to-income ratios are another reason to consider FHA financing. If you carry student loans or other obligations, FHA guidelines provide more flexibility. The program understands that modern borrowers often have legitimate debts while maintaining stable incomes.

The FHA Loan Application Process

Obtaining an FHA mortgage approval typically follows a standard timeline. The loan application process usually takes 30 to 45 days from start to finish. Working with an experienced FHA lender can expedite the process and help avoid delays.

Start by gathering your financial documents. You'll need recent pay stubs, W-2 forms, tax returns, and bank statements. Self-employed borrowers should prepare profit and loss statements to accurately track their financial performance. Having everything organized up front prevents delays during underwriting, which is crucial for those who want to qualify for an FHA mortgage.

Your lender will order an FHA appraisal to assess the property's value and condition. FHA appraisals are more detailed than conventional appraisals. The appraiser checks that the home meets minimum property standards. Issues like peeling paint, broken windows, or roof damage must be repaired before closing.

Pre-approval gives you a clear budget before house hunting. A loan officer reviews your finances and provides a pre-approval letter. This document demonstrates to sellers that you're a serious home buyer with verified financing. Having pre-approval strengthens your offer in competitive markets.

FHA Refinancing Options for Existing Homeowners

Current FHA borrowers have exceptional refinancing opportunities available to them. The FHA Streamline Refinance allows you to lower your interest rate with minimal documentation. You don't need a new appraisal or income verification. This option saves time and money when refinancing.

The FHA cash-out refinance allows you to tap into your home equity. You can borrow up to 80% of your home's current value. This money can be used to fund home improvements, pay off high-interest debt, or cover other expenses. The new mortgage replaces your existing FHA loan.

Refinancing makes sense when rates drop significantly or your financial situation improves. Some homeowners refinance from an FHA mortgage to a conventional loan. This strategy eliminates mortgage insurance once you have sufficient equity. Compare FHA options with conventional refinancing to find the best deal for your needs.

Common Myths About FHA Loans

Misconceptions about FHA financing prevent many qualified borrowers from applying. Understanding the facts helps you make informed decisions. Let's clear up the most common myths about these valuable mortgage products.

The biggest myth is that FHA loans are only for first-time buyers. As we've established, anyone meeting the requirements can qualify. Previous homeowners often use FHA financing when it suits their needs. Your homeownership history doesn't disqualify you from the program.

Another myth claims FHA loans are only for low-income borrowers. Income limits don't exist for standard FHA mortgages. High earners can opt for FHA financing if it offers more favorable terms than alternatives. The program serves borrowers across a range of income levels, including those who qualify for FHA loans for first-time buyers.

Some believe FHA loans take longer to close than conventional mortgages. In reality, closing times are similar. The FHA loan application moves through standard underwriting channels, which can be more favorable for those who meet FHA requirements. Delays typically result from borrower documentation issues rather than the type of loan.

Making Your Decision

Choosing the right home loan requires careful consideration of your options. FHA loans offer flexible financing options for a diverse range of borrowers. Whether you're a first-time homebuyer or an experienced owner, these mortgage products might fit your needs.

Discuss your situation with multiple lenders. Compare interest rates, fees, and loan terms across different programs. An FHA loan could save you money even if you qualify for conventional financing. Run the numbers with a trusted loan officer to determine which option works best for you.

Remember that FHA financing isn't just for beginners. The program welcomes repeat buyers who value flexible requirements and lower down payments. If you've owned a home before, don't assume you're ineligible for an FHA loan again. Check your eligibility and explore this proven path to homeownership.

Connect With Us

Please share – it really helps