FHA Loan Requirements for First-Time Buyers

Buying your first home is an exciting milestone, but it can also be daunting. Mortgages, credit scores, and down payments can make the process seem complicated.

Buying your first home is an exciting milestone, but it can also be daunting. Mortgages, credit scores, and down payments can make the process seem complicated.

That's where FHA loans come in. They’re one of the most popular mortgage programs in the United States, and for good reason. The Federal Housing Administration backs these loans to make homeownership possible for more people, especially first-time buyers.

Let’s walk through everything you need to know about FHA loan requirements for first-time buyers, how the process works, and what it takes to qualify. No stiff jargon. Just the good stuff.

Why FHA Loans Are a Game Changer for First-Time Buyers

FHA loans are intended to assist individuals who may not have a high credit score or substantial savings for a down payment. As these loans are government-insured, lenders are more likely to offer approval.

Even if you’ve had some financial bumps in the road, an FHA loan could still be within reach. The FHA first-time buyer requirements tend to be much more flexible than conventional loan rules. That’s a huge relief when you’re just starting out.

Since 1934, the FHA has helped millions buy homes. Today, the program continues to evolve, with options from condos to small multi-units.

Breaking Down the Core FHA Loan Requirements for First-Time Home Buyers

Before you get too excited, let's go over the basic checklist. Knowing the FHA loan requirements for first-time home buyers upfront will save you time and headaches later.

FHA loans are not limited to first-time buyers, but they are particularly well-suited for first-time buyers. The requirements focus on three factors: credit history, income stability, and property standards.

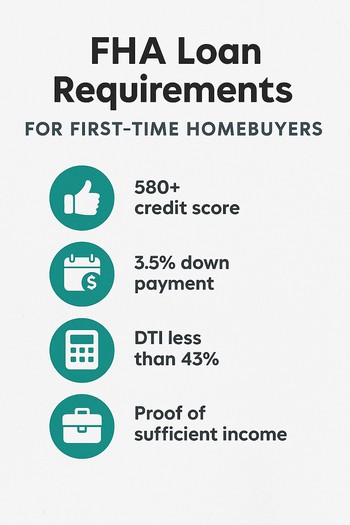

You must live in the home you’re buying. Lenders require at least two years of consistent work or income. All your monthly debts, including the new mortgage, must stay within a set percentage of your income. The home must be FHA-approved based on safety and livability standards.

What about credit scores? Let's get specific.

Credit score requirements for FHA loans depend on the down payment amount. Applicants with a FICO score of 580 or higher are eligible for a 3.5% down payment, which is lower than the minimum required for most conventional loans.

Applicants with a credit score between 500 and 579 may still qualify for an FHA loan if they can provide a 10% down payment. Most lenders prefer scores above 620, which can also improve your chances of a favorable interest rate.

FHA loans require 2 years of credit history. Most lenders prefer a score of 620 or higher, but will consider lower. If you’ve had a bankruptcy or foreclosure, there are waiting periods, though exceptions may apply.

First-Time Home Buyer FHA Loan Requirements: Down Payments and Gift Funds

Let’s talk cash. One of the biggest hurdles for first-time buyers is scraping together a down payment. With first-time home buyer FHA loan requirements, that hurdle gets much lower.

The 3.5% down payment requirement applies to credit scores of 580 or higher. For example, on a $250,000 home, this is $8,750. In comparison, conventional loans typically require a down payment of 5% to 20%.

FHA guidelines permit the use of gift funds from family members, employers, or certain charities for the down payment. If a parent provides the full down payment, a gift letter stating that repayment is not expected is required.

You cannot use borrowed money, such as a personal loan or credit card advance, for your down payment. Down payments must come from your savings, approved gift funds, or FHA-approved programs.

Understanding FHA Loan Limits and Property Rules

FHA doesn't insure just any home at any price. Loan limits vary by county. For 2026, the floor for most single-family homes is around $541,287, but in high-cost areas, it can go much higher.

You can check current limits on the HUD website. Knowing your local limit helps you set a realistic budget. Multi-unit properties (duplexes, triplexes, fourplexes) have higher limits, which is great if you plan to live in one unit and rent out the others.

As for the property itself? FHA appraisers do a thorough inspection. They’re looking for safety issues: working heating, safe drinking water, no lead paint hazards, and structural integrity. If the home has major defects, the seller must fix them before you close.

This inspection protects buyers from purchasing properties with significant issues. It serves as a built-in safety measure.

Mortgage Insurance: The One Downside (But It's Manageable)

All FHA loans include mortgage insurance premiums (MIP). Regardless of the down payment, borrowers pay an upfront premium of 1.75% of the loan amount and an annual premium of 0.45% to 1.05% of the remaining loan balance.

The upfront MIP can be financed as part of the loan, eliminating the need to pay it at closing. The annual premium is divided into monthly installments.

With a down payment below 10%, mortgage insurance premiums are required for the duration of the loan. However, once sufficient equity (typically 20% or more) is established, refinancing to a conventional loan may eliminate mortgage insurance.

Many buyers choose to refinance after a few years, particularly if their home value increases. FHA loans can serve as a transitional option before moving to a conventional mortgage.

Debt-to-Income (DTI) Ratios: What You Can Actually Afford

Lenders must confirm your ability to manage the monthly payments. FHA reviews two primary ratios:

- Housing ratio (front-end): Your mortgage payment (principal, interest, taxes, insurance) shouldn’t exceed 31% of your gross monthly income.

- Total debt ratio (back-end): Your mortgage plus all other debts (car loans, student loans, credit cards) should stay below 43% of your gross monthly income.

These guidelines are flexible. Substantial savings, an extended employment history, or minimal credit card debt can be viewed as compensating factors. With these, some lenders may accept higher debt-to-income ratios, up to 57%.

When you apply, you’ll need to document income with pay stubs, W-2s, and tax returns. Self-employed? You’ll need additional paperwork, such as profit-and-loss statements. Overtime and bonus income count if you can show a two-year history.

The FHA Loan Application Process: Step by Step

The following are the typical steps for fulfilling FHA loan first time buyer requirements:

- Step 1: Find an FHA-approved lender. Not every lender offers FHA loans. Check first.

- Step 2: Get pre-approved. This tells you how much home you can afford. You’ll share income, assets, and credit info. Pre-approval also makes your offer stronger in a competitive market.

- Step 3: House hunt & make an offer. Work with a realtor who knows FHA transactions.

- Step 4: Complete full application & submit documents. Pay stubs, bank statements, tax returns, ID, etc.

- Step 5: Underwriting & appraisal. The lender orders an FHA appraisal. The underwriter reviews everything and may ask for conditions.

- Step 6: Clear to close & closing day. Sign papers, get keys, move in!

The process generally takes 30 to 45 days. Promptly responding to document requests helps ensure timely progression.

Special FHA Loan Programs You Should Know About

The standard FHA loan is great, but there are specialized versions too:

- FHA 203(k) loan: Buy a fixer-upper and roll renovation costs into one mortgage. Perfect if you’re handy or want to build sweat equity.

- FHA manufactured home loan: For mobile or modular homes on permanent foundations.

- Energy-efficient mortgage (EEM): Finance upgrades like solar panels or new insulation.

- Home Equity Conversion Mortgage (HECM): A reverse mortgage for homeowners 62+.

For first-time buyers considering a property that requires renovation, the 203(k) loan may be beneficial.

Frequently Asked Questions (FAQs)

Can I get an FHA loan with a credit score below 580?

Yes, but you'll need a 10% down payment. And you'll have to find a lender who accepts scores as low as 500. Many lenders prefer a credit score of 580 or higher, so you may need to shop around. The FHA itself allows it, but individual lenders can set their own "overlays" (stricter rules).

What's the minimum down payment for an FHA loan?

If your credit score is 580 or above, the minimum down payment is 3.5%. If your score is between 500 and 579, the minimum is 10%. Remember, down payment gifts from family are allowed, which is a huge help for many first-time buyers.

How long does FHA mortgage insurance last?

If you put down less than 10%, you'll pay annual MIP for the entire loan term (usually 30 years). If you put down 10% or more, MIP drops off after 11 years. The only way to remove it early is to refinance into a conventional loan.

Can I use an FHA loan to buy a duplex or triplex?

Absolutely. FHA loans cover 1-4 unit properties. You must live in one unit as your primary residence. The rental income from the other units can help you qualify for a larger loan amount. It's a smart strategy for first-time buyers looking to offset their mortgage payments.

Are FHA loans only for first-time home buyers?

Nope! While they're incredibly popular with first-timers, repeat buyers can use FHA loans too. However, you generally can't have more than one FHA loan at a time unless you're relocating for work or have other approved circumstances. So if you already own a home with an FHA loan, you'll likely need to sell it or refinance before getting another.

Putting It All Together: Your Path to Homeownership

FHA loans aren't just a financial product—they're a real opportunity. For millions of Americans, meeting FHA loan requirements for first-time home buyers has made the dream of owning a home a reality. Yes, there's mortgage insurance. Yes, there are property standards. But the flexibility is unmatched.

Start by checking your credit score. Then, gather your pay stubs and bank statements. Reach out to a few FHA-approved lenders and compare rates. Ask about current loan limits in your county. And don't be afraid to ask "dumb" questions—that's how you learn.

The FHA program has been helping people just like you since 1934. It's proven, it's solid, and it's waiting for you to take that first step. Go tour a few open houses. Picture your key in that front door. You've got this.

Connect With Us

Please share – it really helps