Pros and Cons of FHA Loans

When

exploring home financing options, many borrowers find themselves

weighing different loan types. FHA loans represent one of the most

popular choices for first-time homebuyers and those with

less-than-perfect credit, as they often qualify for an FHA loan more

easily. These government-backed mortgages offer unique advantages

but also come with specific drawbacks that every potential homeowner

should understand.

When

exploring home financing options, many borrowers find themselves

weighing different loan types. FHA loans represent one of the most

popular choices for first-time homebuyers and those with

less-than-perfect credit, as they often qualify for an FHA loan more

easily. These government-backed mortgages offer unique advantages

but also come with specific drawbacks that every potential homeowner

should understand.

FHA loans help millions of Americans achieve homeownership each year. The Federal Housing Administration backs these mortgages, making them less risky for lenders and more accessible for borrowers. However, like any financial product, FHA loans include both benefits and limitations that can impact your long-term economic health.

Understanding the pros and cons of FHA financing can help you make an informed decision about your home purchase and whether to refinance into a conventional loan later. This guide provides an in-depth look at everything you need to know about FHA loans, from their flexible requirements to their potential drawbacks.

What Makes FHA Loans Different

FHA loans differ from conventional mortgages in several key ways. The Federal Housing Administration insures these loans, which means lenders face less risk when approving borrowers. This insurance protection allows lenders to offer more flexible qualification standards and lower payment requirements.

These government-backed mortgages typically require a minimum credit score of 580 for the lowest payment option. Borrowers can qualify with a score as low as 500 if they put more money up front. This flexibility makes FHA loans attractive to borrowers who might not meet conventional loan standards.

The debt-to-income (DTI) ratio requirements for FHA loans also offer more leniency than traditional mortgages. Borrowers can qualify with a DTI ratio up to 57% in some cases, though most lenders prefer ratios below 43%. This flexibility helps borrowers with higher debt loads secure financing, making it easier for them to apply for an FHA loan.

FHA loans allow borrowers to receive gift funds from family members for their payment and closing costs. This feature makes homeownership more accessible for buyers who may not have substantial savings but have supportive family members willing to provide financial assistance.

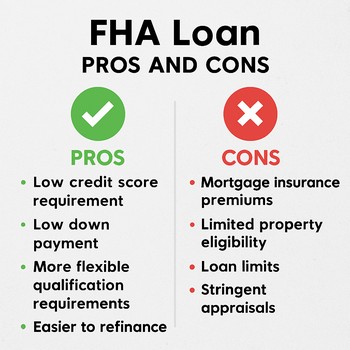

- FHA loans offer flexible credit score requirements starting at 580, making it easier for many to apply for an FHA loan.

- Borrowers can use gift funds from family for payment and closing costs, which is a significant advantage when considering how to get an FHA loan.

- DTI ratios can go higher than conventional loan requirements

- Government backing reduces lender risk and increases approval chances

Benefits of FHA Loans That Help Borrowers

The primary advantage of FHA financing lies in its accessibility. These loans make homeownership possible for borrowers who might not qualify for conventional financing. The lower credit score requirements open doors for buyers working to rebuild their credit history after experiencing financial difficulties, making it easier for them to qualify for an FHA loan.

FHA loans require as little as 3.5% for a payment when borrowers have credit scores of 580 or higher. This low payment requirement helps buyers enter the housing market sooner rather than waiting years to save a larger amount. For many families, this difference represents the key to achieving homeownership and helps them qualify for an FHA loan.

The flexible income requirements of FHA loans accommodate various employment situations. Borrowers can include income from multiple sources, including part-time work, alimony, and even student loan payments in certain circumstances. This flexibility helps self-employed individuals and those with non-traditional income streams qualify for financing.

FHA loans also offer benefits during the refinance process. The FHA Streamline Refinance program allows borrowers to refinance their existing FHA mortgage with minimal documentation and, in many cases, no appraisal requirement. This option helps homeowners secure lower interest rates without the hassle of a complete application process.

Another significant benefit involves the assumable nature of FHA loans. When interest rates rise, buyers can potentially assume the seller's existing FHA loan if they meet qualification requirements. This feature can provide substantial savings in higher-rate environments.

These mortgages also include provisions for borrowers facing financial hardship. FHA lenders offer various workout options, including loan modification and forbearance programs, to help borrowers avoid foreclosure during difficult times.

Disadvantages of FHA Loans to Consider

While FHA loans offer many benefits, they also include several disadvantages that borrowers must weigh carefully. The most significant drawback involves mortgage insurance requirements that increase monthly payments and overall costs.

FHA loans require two types of mortgage insurance premium payments. Borrowers pay an upfront mortgage insurance premium (UFMIP) of 1.75% of the loan amount at closing. Additionally, they must pay an annual premium that ranges from 0.45% to 1.05% of the loan amount, depending on the loan type and payment amount, which are important factors to weigh when considering the pros and cons of FHA loans.

Unlike conventional loans, FHA mortgage insurance premium payments continue for the life of the loan in most cases. Borrowers who put less than 10% typically cannot remove this insurance, even when they reach 20% equity. This requirement means higher monthly payments throughout the entire loan term.

Property standards for FHA loans can also present challenges. These mortgages require properties to meet specific safety and habitability standards that exceed typical conventional loan requirements. Homes must pass an FHA appraisal, which examines both value and condition. Properties that require significant repairs may not qualify for FHA financing, which is a con of an FHA loan that potential borrowers should consider.

FHA loan limits vary by area and may restrict options in higher-cost housing markets. These limits determine the maximum amount borrowers can borrow through the FHA program. In expensive areas, these limits may fall below median home prices, forcing buyers to consider other financing options.

- FHA loans require both upfront and annual mortgage insurance premiums

- Insurance premiums typically cannot be removed during the loan term

- Properties must meet strict FHA appraisal and safety standards

- Loan limits may restrict options in high-cost housing markets, which is a con of an FHA loan that should be taken into account.

FHA vs Conventional Loan Comparison

Understanding the differences between FHA and conventional loans helps borrowers make informed decisions. Conventional mortgages offer advantages that may benefit specific buyers, while FHA loans serve others better based on their financial situation and goals.

Conventional loans typically require higher credit scores, usually starting around 620 for most lenders. However, they offer the ability to remove private mortgage insurance once borrowers reach 20% equity, a significant pro when deciding to get an FHA loan. This feature can result in substantial monthly payment savings over time.

The payment requirements for conventional loans vary, but can be as low as 3% for qualified borrowers through specific programs. However, borrowers putting less than 20% must pay private mortgage insurance, which adds to monthly costs but can be removed later.

Interest rates on conventional loans may be slightly lower than those on FHA loans for borrowers with excellent credit. However, FHA rates remain competitive and may actually be lower for borrowers with credit scores below 640.

Conventional loans offer more flexibility in property types and locations. These mortgages can finance condominiums, investment properties, and higher-priced homes without the restrictions that apply to FHA financing. Borrowers seeking luxury homes or investment properties typically need conventional funding.

The application process for conventional loans may be more streamlined for well-qualified borrowers. However, FHA loans offer more flexibility in documenting income and assets, which can benefit self-employed borrowers or those with complex financial situations.

Borrowers with strong credit scores and substantial savings often find conventional loans more cost-effective in the long term. The ability to remove mortgage insurance and potentially secure lower rates can result in significant savings over the life of the loan.

Who Benefits Most from FHA Loans

FHA loans are best suited for specific types of borrowers who can effectively leverage their advantages while minimizing their disadvantages. First-time homebuyers often find these loans particularly attractive due to their accessible requirements and educational resources.

Borrowers with credit scores between 580 and 640 typically find better options with FHA financing than conventional loans. The flexible credit requirements and competitive rates make FHA loans more accessible for this credit range.

Self-employed individuals and those with non-traditional income sources may find FHA loans easier to qualify for than conventional financing. The flexible documentation requirements can accommodate various income types that traditional lenders might reject.

Buyers in lower to moderate-cost housing markets can take full advantage of FHA loan benefits without hitting loan limits. These borrowers can access affordable financing while staying within program parameters.

Military families and veterans should compare FHA loans with VA loan benefits. While VA loans offer superior terms for eligible borrowers, FHA loans provide an alternative for those who don't qualify for VA financing or want to preserve their VA eligibility for future use.

Borrowers planning to stay in their homes for many years may find the long-term costs of FHA mortgage insurance less concerning when they weigh the pros and cons of an FHA loan. The stability and accessibility of FHA financing can outweigh the higher costs for long-term residents.

- First-time homebuyers benefit from FHA educational resources and flexible requirements

- Borrowers with credit scores of 580-640 often find better FHA options than conventional loans

- Self-employed individuals appreciate flexible income documentation requirements

- Long-term homeowners may find that FHA benefits outweigh mortgage insurance costs

Making Your FHA Loan Decision

Choosing between FHA and conventional financing requires careful analysis of your financial situation, goals, and local market conditions. Consider your credit score, available funds for payment, and long-term homeownership plans when evaluating options.

Calculate the total cost of each loan type over your expected ownership period. Include mortgage insurance costs, interest rates, and any potential savings from removing insurance or refinancing. This analysis helps determine which option provides better value for your situation, allowing you to weigh the pros and cons of FHA loans effectively.

Read about current market conditions and interest rate trends before applying. Rising rates may make assumable FHA loans more attractive, while falling rates might favor conventional financing with its flexibility to remove mortgage insurance.

Work with experienced lenders who can explain the differences between loan types and help you understand which option best fits your needs. Many lenders offer both FHA and conventional loans, allowing you to compare options side by side.

Consider your plans for the property. If you expect to refinance or sell within a few years, the ability to remove mortgage insurance on conventional loans may not provide significant benefits. However, if you plan to stay long-term, this feature could save thousands.

Start your application process early to give yourself time to explore different options. Pre-approval letters help you understand what you qualify for and make your offers more competitive in today's market.

FHA loans continue to serve millions of borrowers successfully each year. These government-backed mortgages provide a pathway to homeownership for many who might otherwise struggle to qualify. However, they work best when borrowers understand both their advantages and limitations.

The decision between FHA and conventional financing depends on your unique financial situation and homeownership goals, particularly when considering whether to apply for an FHA loan. By understanding the pros and cons of each option, you can make an informed choice that supports your long-term economic health and homeownership dreams

Connect With Us

Please share – it really helps