FHA Loans for First-Time Homebuyers Explained Clearly

I've worked with thousands of first-time homebuyers, and one mistake

stands out.

I've worked with thousands of first-time homebuyers, and one mistake

stands out.

It's not about credit score or savings - it's about rushing into an FHA loan without knowing its long-term impact.

Allow me to be clear: the FHA home Buyers' program is an effective tool. But it's not always the right fit for everyone.

These loans are backed by the Federal Housing Administration. That backing lowers lenders' risk, allowing more people to qualify.

As a first-time buyer, FHA is not your only choice, but it is one of the most flexible.

FHA loans are for buyers with imperfect credit or a limited down payment payment. They can unlock options conventional loans may not offer. If you're a first-time buyer, This program deserves a serious look.

Let's walk through how they really work. No specialized terms. No nonsense. Just the honest breakdown I wish every first-time buyer had upfront. First, let’s look at what makes FHA loans uniquely advantageous for new buyers.

First-Time FHA Loan Advantages Explained Clearly:

FHA loans offer first-time buyers lower down payments and more relaxed credit requirements than conventional loans.

That flexibility can be a breakthrough. You don't need perfect finances to take this step.

Here's what stands out most for first-time buyers, especially those Exploring the FHA home buyers program for the first time:

- Minimum down payment: 3.5%

- Credit scores as low as 580 (sometimes lower with certain lenders)

- Gift funds allowed for the entire down payment.

- Higher debt-to-income ratios are accepted in comparison to conventional loans.

Imagine you've saved $25,000. With a conventional loan, you might be Looking at modest homes in lower price ranges.

But with FHA support, that same $25,000 could stretch further. You might qualify for a home that's significantly more expensive.

Such flexibility can expand your home selection power. It gives you options you wouldn't have otherwise.

However, greater buying power also means long-term costs. The key trade-off is qualifying more easily now, but paying mortgage insurance over time.

You're trading lower upfront requirements for ongoing monthly expenses. Understand the trade before you sign.

FHA Mortgage Insurance Costs Explained Clearly

Mortgage insurance is one of the most misunderstood parts of the FHA loans. I see buyers overlook it all the time.

Every FHA loan includes mortgage insurance, added to each monthly payment.

There are actually two types of FHA mortgage insurance:

- Upfront mortgage insurance premium (UFMIP): 1.75% of the loan amount, paid at closing

- Annual mortgage insurance premium (MIP): Paid monthly, typically 0.45% to 1.05% of the loan

Allow me to give you a real example. On a $300,000 home with 3.5% down, Your loan amount would be about $289,500.

The upfront premium alone would add roughly $5,066 to your closing costs. That often surprises buyers who have only focused on the down payment.

Then you've got the monthly premium. That can easily add $100 to $250 per month, depending on your loan terms.

Here's the catch: unlike conventional loans, FHA mortgage insurance does not automatically disappear at 20 percent equity. Not even close.

For most FHA loans, if you put down less than 10%, mortgage insurance lasts for the life of the loan. The only way out is refinancing into a conventional loan.

That's a big deal. Make sure you understand it before you commit.

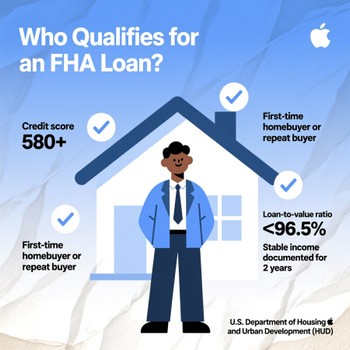

FHA Credit Score Rules and Lending Standards

The FHA allows lower credit scores than traditional mortgages. But Here's what people get wrong.

Lenders are often stricter than the FHA minimums. The agency might say "500 with 10% down," but most banks won't touch that.

Here are the real-world guidelines most lenders follow:

- Ideal minimum credit score: 580 for 3.5% down

- Acceptable range: 500-579 requires 10% down

- Many lenders look for a score of 620 or higher for smoother approval.

Approval depends more on recent credit behavior than the score itself. A 620 with a clean recent history beats a 650 with late payments last month.

A clean payment history over the last two years is more important than older financial errors. Lenders want stability, not perfection.

They're searching for patterns. Have you paid your rent on time? Your car loan? Your credit cards? That real behavior matters more than a three-digit number.

If you've had past issues, but you've been solid for 12-24 months, You're in a good spot. If you have recent late payments or collections, it might be worth waiting.

What If my credit score is below 580?

You still have options, but they're more limited. You would likely need a 10% down payment instead of 3.5%.

Some smaller lenders and credit unions offer more flexible programs. It's worth shopping around if you're in this range.

But honestly? You might be better off spending six months improving Your credit first. A higher score saves you thousands in the long run.

FHA Loan Limits and Borrowing Power Rules

FHA loan limits define the maximum amount you can borrow in each county. These limits vary based on local housing costs.

For most of the country, here are the standard FHA loan limits for 2026:

| Single-family | $541,287 |

|---|---|

| Duplex (2 units) | $693,050 |

| Tri-plex (3 units) | $837,700 |

| Four-plex (4 units) | $1,041,125 |

For 2026, the FHA ceiling was set at $1,249,125 for a single-family home loans. This represents the maximum amount a borrower can obtain through the FHA loan program. It applies to high-cost areas in the United States and is illustrated in the table below.

If you live in an expensive market like San Francisco, New York City, or Washington, D.C., these high-cost limits will apply to you:

| Single-family | $541,287 |

|---|---|

| Duplex (2 units) | $693,050 |

| Tri-plex (3 units) | $837,700 |

| Four-plex (4 units) | $1,041,125 |

But here's what nobody tells you: you can't automatically qualify for the maximum limit just because it exists. Lenders also look at your debt-to-income ratio.

Most FHA lenders require a debt-to-income ratio between 43% and 50%. That means your total monthly debts (including the new mortgage) shouldn't exceed about half your gross monthly income.

A high loan limit is of little use if your monthly income cannot support the payment. Affordability always overrides borrowing ceilings.

I've seen buyers qualify for $400,000 but only feel comfortable at $280,000. That's smart. Don't let a high limit trick you into overextending yourself.

Your comfort matters more than a lender's maximum approval. Trust your Get on what payment fits your life, not just the theoretical budget.

FHA Loan Application Process Schedule Steps

FHA loan applications follow a structured approval procedure. Most Loans close within 30 to 45 days of application.

Here is the basic timeline you can expect:

- Week 1-2: Application and initial document gathering

- Week 2-3: Lender orders appraisal and begins underwriting

- Week 3-4: Appraisal completed, any conditions requested

- Week 4-6: Final approval and closing

Applicants must provide tax returns, pay stubs, bank statements, and employment records. Missing any of these slows everything down dramatically.

Even small issues can delay approval. Unexplained deposits. Incomplete pages. Missing signatures. Outdated statements. All of it matters.

My advice? Get every document ready before you even apply. Have two months of bank statements, two years of tax returns, and your last 30 days of pay stubs.

Preparation is the single biggest factor for a smooth process. The buyers who have everything ready at day one close two weeks faster than those who don't.

FHA Appraisal Rules for Homebuyers Explained

FHA appraisals focus heavily on property safety and condition. This is different from a conventional appraisal, which primarily focuses on the market value.

Homes must meet minimum livability standards called HUD's "Minimum Property Requirements." These cover safety, security, and soundness.

What do appraisers actually look for? Here are common deal-breakers:

- Peeling or chipping paint (lead-based paint hazard)

- Missing handrails on stairs

- Cracked or broken windows

- Leaking roofs or visible water damage

- Faulty electrical or plumbing systems

- Evidence of termites or pest infestation

Older homes often require repairs before approval. That $200,000 A fixer-upper might seem like a steal, but if the appraisal flags structural issues, the deal could fall apart fast.

Sellers aren't always willing to make those repairs. And as a buyer, You can't waive the FHA appraisal or repair requirements.

If repairs are not completed before closing, the deal dies. Property condition directly affects your financing eligibility, sometimes in ways you can't negotiate around.

FHA vs Conventional Loan Comparison Guide

FHA and conventional loans serve completely different financial situations. Neither is universally better. It all depends on your specific numbers.

Allow me to break down when each one makes sense.

FHA is often better when:

- Your credit score is between 580 and 620

- You have a small down payment (3.5% to 5%)

- You have higher existing debt relative to income.

- You've had a past bankruptcy or foreclosure.

Conventional loans may be better when:

- Your credit score is 620 or higher (ideally 660+)

- You can put down 5% to 10%

- You want mortgage insurance to drop off automatically once you reach 20% equity.

- You plan to stay in the home for many years.

The biggest hidden difference is mortgage insurance. With a With a conventional loan, you can request removal at 20% equity, while with an FHA loan A loan is usually permanent unless you refinance.

Comparing total long-term costs is essential before deciding. Monthly Savings today may look great, but lifetime costs might tell a different story story.

Run the numbers both ways. A good lender will show you a side-by-side comparison. If they won't, find another lender who will.

FHA Loan Mistakes First-Time Buyers Make

First-time buyers often make emotional financial decisions. I've seen the same mistakes hundreds of times.

These mistakes can reduce your long-term economic security. Avoid them, and you'll be way ahead of most buyers.

Mistake #1: Shopping with only one lender

Different lenders offer different terms and approval flexibility. Rates vary. Fees vary. Even credit requirements vary. Always compare at At least three lenders.

Mistake #2: Borrowing the maximum limit

Just because the bank says you qualify doesn't mean you should take it. High payments quickly strain monthly budgets. Leave yourself breathing room.

Mistake #3: Ignoring mortgage insurance costs

That $200 monthly premium adds up to $2,400 per year. Over five years, That's $12,000 you could have put toward principal. Plan for the full payment structure.

Mistake #4: Not checking your credit before applying

Pull your credit reports three to six months before house hunting. You need time to fix errors or pay down balances. Don't discover problems mid-application.

Mistake #5: Changing jobs during the process

Lenders want stability. Switching jobs, even for more money, can derail approval. Wait until after closing if possible.

When FHA Loans Are Not Ideal Options

FHA loans are not suitable for every financial situation. Sometimes The best move is to wait and strengthen your position first.

Here are clear signs an FHA loan might not be right for you right now:

- You have had recent late payments or collections (within the last 12 months)

- You started a new job in a different field within the last six months.

- Your debt-to-income ratio exceeds 50%, even with FHA flexibility.

- You have the credit and down payment for a conventional loan with reduce long-term costs.

- You're looking at a fixer-upper that won't pass an FHA appraisal.

Low credit scores with recent negative marks often require waiting periods. A foreclosure typically needs three years. A bankruptcy takes 2 years (sometimes 1 for Chapter 13 with court approval).

New jobs or unstable income can weaken applications, too. Lenders want to see at least two years of consistent employment in the same field.

Strengthening your financial history frequently leads to better results later. Waiting six to twelve months might save you thousands on a mortgage insurance and get you a better rate.

Sometimes the best loan is the one you don't take yet. Patience pays off in real estate more than almost anything else.

Frequently Asked Questions

What credit score is needed for FHA approval as an FHA first-time buyer?

Most FHA loans require a credit score of at least 580. That's the sweet spot for the 3.5% down payment option. Some lenders may require higher scores, typically 620 to 640, depending on their internal risk guidelines. If your score is between 500 and 579, you can still qualify, but you'll need a 10% down payment.

As an FHA first-time buyer, Don't assume you need perfect credit. Many first-timers qualify with scores in the low 600s.

How What down payment is required for an FHA loan under the FHA first home buyer program ?

FHA loans typically require a 3.5 percent down payment if your credit score is 580 or higher. That's $10,500 on a $300,000 home. Gift funds may also be used for the entire down payment, provided they are properly documented with a gift letter and proof of funds transfer. No waiting period is required for gifted funds with FHA loans. For anyone using the FHA first-time homebuyer path, this low down payment is often the biggest draw.

Do Do FHA loans require mortgage insurance?

Yes, all FHA loans include mortgage insurance in monthly payments. There's no way around it. For loans with less than 10% down, that insurance usually remains for the life of the loan unless you refinance into a conventional product. Even with 10% or more down, you'll pay mortgage insurance for at least 11 years. The FHA home buyers program is transparent about this cost, but many buyers still underestimate it.

How How long does an FHA loan approval take for an FHA first-time homebuyer?

FHA loan approval usually takes 30 to 45 days from application to closing. Delays often come from missing documents or appraisal issues. The fastest approvals happen when buyers submit complete tax returns, bank statements, pay stubs, and ID forms on day one. Understaffed lenders or busy seasons can stretch this to 60 days. If you're an FHA first-time Homebuyer, ask your lender upfront about their current turnaround times.

Can first-time buyers use FHA loans through the FHA Home Buyers Program?

Yes, FHA loans are specifically designed for first-time buyers. The The FHA home buyers program offers flexible credit and lower down payment options that make that first purchase possible. There's no requirement to be a first-time buyer, though - Repeat buyers can use FHA, too, as long as they plan to live in the home as their primary residence. That said, most FHA borrowers are indeed first-timers.

Can I use an FHA first-time homebuyer loan for a condo or townhouse?

Yes, but the condo complex must be on the FHA-approved list. Not all condos qualify. Your lender can check the HDA (HUD Developer Approval) database to see if the complex is approved. If it's not, you may need to go with a conventional loan or ask the condo association to pursue FHA certification. Many FHA first home buyer applicants are surprised by this rule, so check before you fall in love with a condo.

What's the difference between an FHA first-time homebuyer and a conventional homebuyer loan?

As an FHA first-time homebuyer, You'll typically get easier credit requirements and a lower down payment with FHA. However, you'll pay mortgage insurance for much longer. Conventional loans might require a slightly higher credit score and down payment payment, but your monthly costs could be lower over time if you have good credit. Every buyer's situation is different. Run both scenarios before deciding which path best fits your finances.

Connect With Us

Please share – it really helps